A decade ago in March 2014, then chancellor George Osborne, uttered some momentous words: “Let me be clear. No one will have to buy an annuity.”

It didn’t make much sense to me in the moment. I’m not talking about the policy, just the words. At the time I worked for Hargreaves Lansdown, and we had offered drawdown, without advice, for the best part of a decade. So, in truth, no one had to buy an annuity before or after the chancellor’s Budget speech.

But it’s the optics that mattered. As a result of the pension freedoms, annuity sales, and the share price of many annuity providers, fell off a cliff.

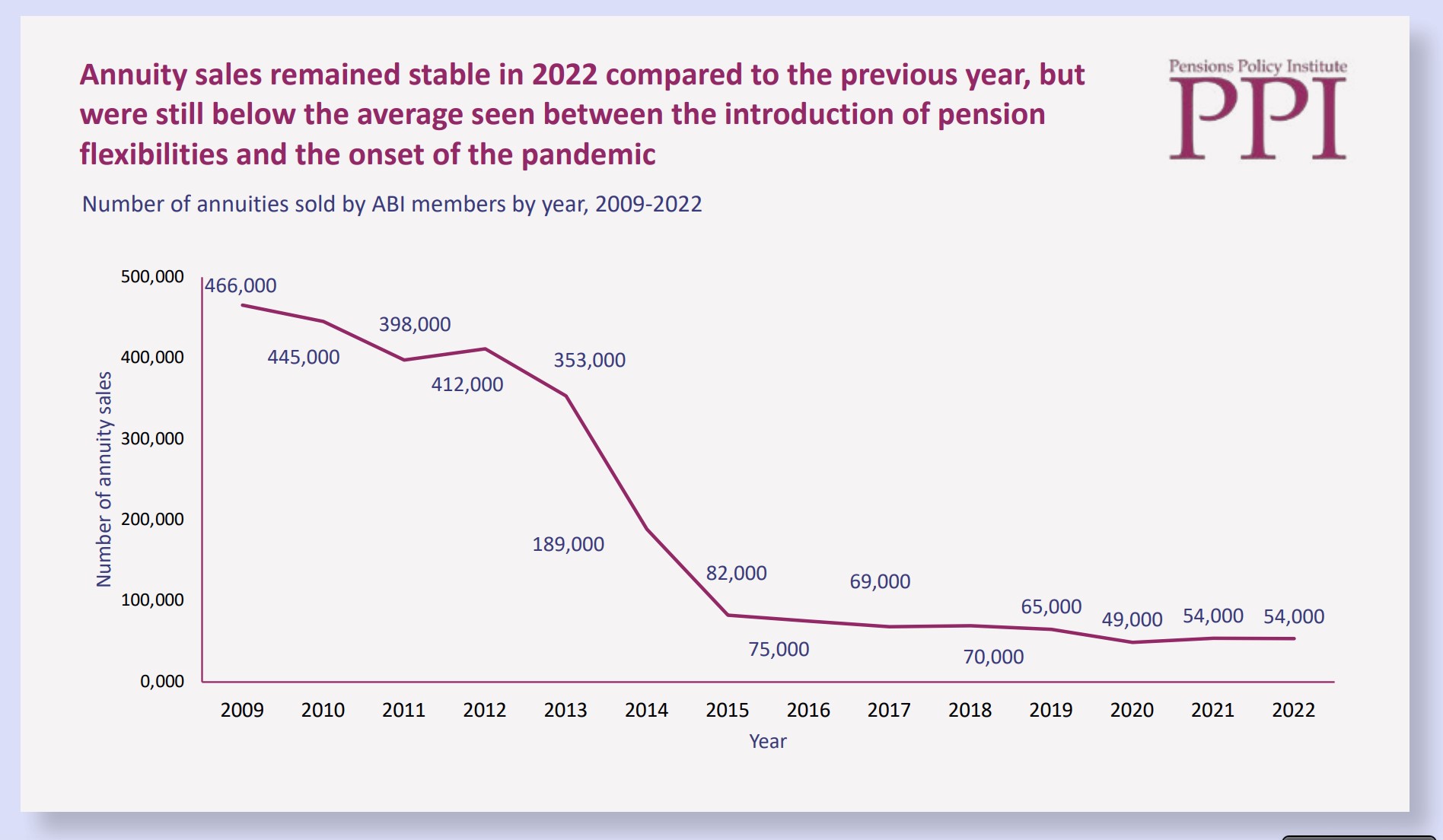

Annuity sales data from the ABI in the most recent PPI DC Future Book illustrates this perfectly:

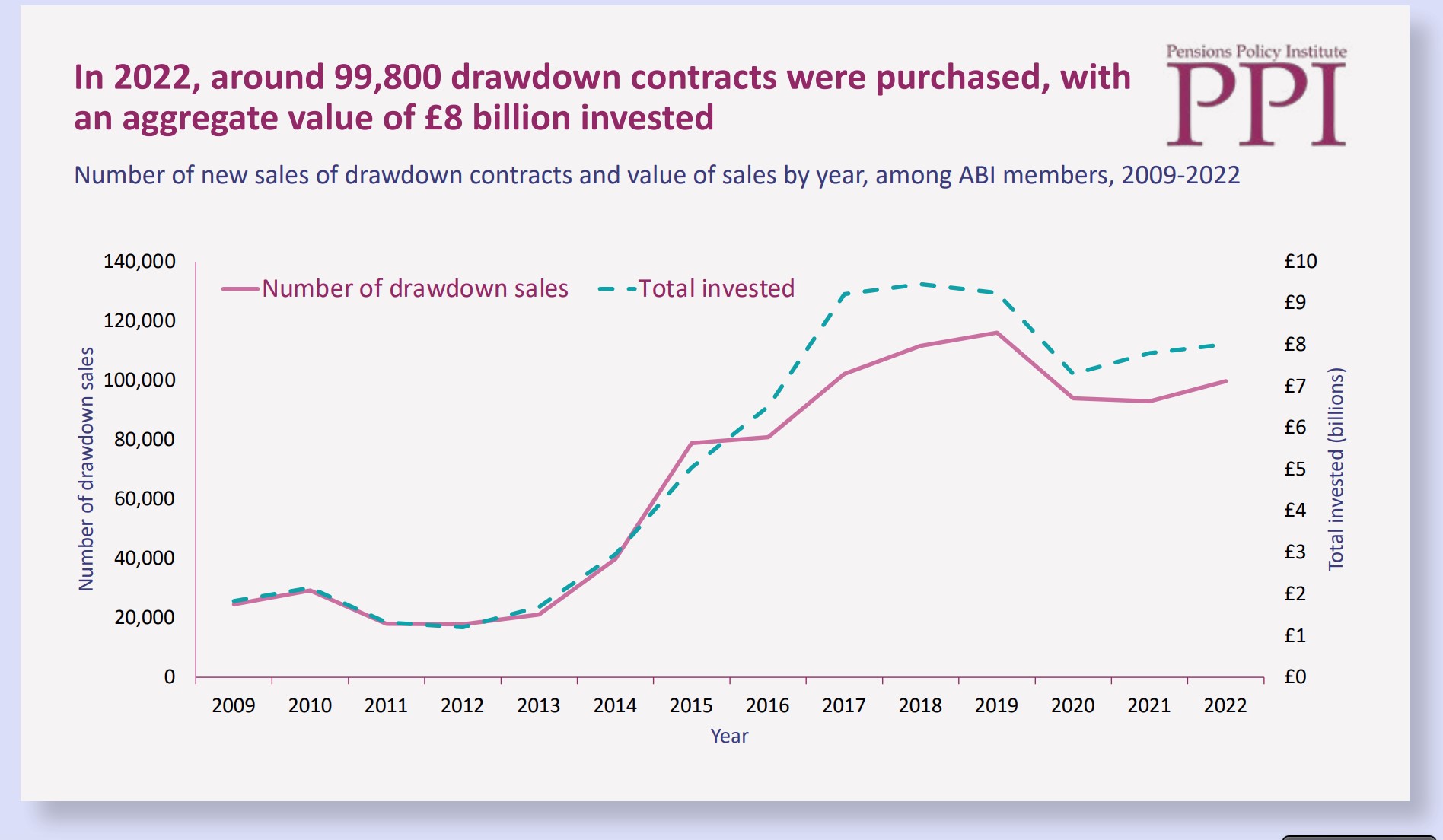

Over the same period, drawdown sales and the total value invested in drawdown went in the opposite direction:

The chancellor’s announcement blindsided markets, pension professionals and even the FCA and TPR. Since then, regulators have been playing catchup.

To try and keep a handle on things, the FCA requires the firms they regulate to submit data on how customers are accessing their pensions.

The latest iteration of this data was released in April. Before sharing the insights of note for employers, let’s start by confirming what it doesn’t show us:

Whether people are taking a sustainable income

Fundamentally, this data can only ever be partial. Despite the buzzy adverts you see on buses about how easy it is to consolidate pensions, most people tend to have multiple pots.

The FCA data looks at pensions not people. So when it says the most popular withdrawal rate for pensions worth less than £10,000 is over 8%, we have no idea how much their other pensions are worth.

Whole of market data

The FCA only regulate contract-based pensions. This means they’re not collecting data on trust-based pensions. And TPR doesn’t collect similar data to give us a whole-of-market overview.

Whilst it’s still rare for trust-based pension to offer drawdown, most now offer partial- and full- lump sum withdrawal. So we’re not getting the full picture.

The future

Today’s retirees are nothing like tomorrow’s. Many benefited from DB pension accrual for much of their careers. Whilst others missed out on the DB-lucky-dip and saved very little due to automatic enrolment not being in place for most of their careers.

Retirees of the future will have larger DC pensions and less of a DB safety net. So they’re likely to access their pensions very differently.

But enough of what it doesn’t show. Here are my top three highlights from the latest data worth considering when making decisions on behalf of you pension members, and why they matter:

- The total number of pension plans accessed for the first time in 2022/23 increased by 5% to 739,535, vs. 2021/22.

2022 was the year that rent, mortgages and the general costs of living started to rise. For those over 55, tapping into pension savings may have been a welcome pressure release valve.

- 57% of those plans were accessed via full fund withdrawal.

People in the industry often talk about how drawdown has become the flagship retirement option. But the data just doesn’t show that. The norm is to cash-in your pension and take everything out in one go. Why?

There’s lots of good reasons to take money out of your pension – pay off the mortgage, clear expensive debts, have a great holiday – but many people do it because they don’t trust pensions and want the money in their bank account, despite the tax implications.

- Sales of annuities decreased by 14%

This was the biggest surprise for me. Movements in the gilt market in 2022 meant annuity rates increased significantly. Best buy rates for a 65 year old show that rates went from around 5.5% to 6.7% during the reporting period (a 22% increase). But this didn’t mean there was a rush to lock in a secure income for life.

A friend of mine, Mark Ormston, who works for Retirement Line (an annuity broker) thinks that we’ll see these rate rises boost annuity purchases in next reporting period. We’ll have to wait and see!

All in all, an interesting set of data, despite the earlier caveats about what the data can’t show us.

And now the FCA have been collecting data in the same way since 2018, we’re starting to understand long-term trends. It’ll be interesting to see how these develop as the DC market matures.